Perspectives

From Access to Accountability: The Next Chapter in Behavioral Health

Behavioral health has long represented one of the largest gaps between disease burden and care delivery in the U.S. health system. Nearly one in four American adults — 61.5 million people — experienced a mental health condition in 2024, with of that population also meeting criteria for a substance use disorder. Yet nearly half of those with a mental health condition received no treatment, and fewer than one in five of those needing substance use treatment received it. The economic cost is staggering: $282 billion in annual productivity losses, direct expenditures, and suicide-related costs, and $477.5 billion in avoidable costs attributable to unaddressed mental health inequities, with projections of $14 trillion in cumulative costs through 2040.

COVID-19 forced these gaps into the open. Anxiety and depression prevalence roughly tripled during the pandemic, and within two years, hundreds of digital behavioral health platforms had launched on the premise that technology could close the access gap at scale. Capital flooded in: digital mental health companies raised $4.9 billion in 2021 alone, while behavioral health remained the single most funded clinical indication in digital health every year from 2020 through 2024. The access gap was real, and investor conviction was justified.

This next chapter for digital behavioral health is about moving beyond access – toward accountability, outcomes, and the clinical infrastructure to sustain both. Behavioral health platforms – formed during or shortly after the pandemic – made real progress across several fronts: reducing stigma, dismantling geographic barriers, and reaching underserved populations for the first time. At the same time, utilization growth across the broader sector outpaced meaningful clinical outcomes and population-level ROI remained difficult to verify. The same structural barriers that defined the problem before the pandemic — a worsening provider shortage, fragmented care, and overlap with chronic physical conditions — proved resistant to change at scale.

The Structural Challenges That Remain

The behavioral health system’s persistent challenges are not accidental. They reflect structural misalignments that technology-enabled access alone cannot resolve.

The provider shortage is getting worse, not better. HRSA projects a shortfall of more than 43,000 psychiatrists and 77,000 addiction counselors by 2038. More than 60% of active psychiatrists are aged 55 or older and are likely to retire in the next 10-15 years. No training pipeline adjustment closes this gap on any near-term timeline. Virtual therapy still requires licensed therapists — and the same shortage that constrained in-person care constrained virtual care at scale. The most scalable near-term lever is technology that extends what existing providers can do, not technology that tries to bypass them.

Behavioral health’s overlap with chronic physical conditions compounds the challenge. Individuals with mental illness have two to three times the rate of comorbid conditions including diabetes, hypertension, and cardiovascular disease. Comorbid behavioral-physical populations are among the highest per-member cost segment across payers with healthcare costs running 2.8 to 6.2 times higher, and this population accounting for more than 56% of all healthcare costs despite representing only 27% of insured lives. Managing these populations in clinical and administrative silos is both clinically incoherent and economically inefficient.

At the same time, rapid expansion of digital behavioral health during the pandemic exposed structural gaps the sector is still working through. While some platforms built meaningful payer relationships, many entered the market through direct-to-consumer or self-pay channels, limiting their reach within the broader healthcare system. Outcome measurement varied widely: some platforms invested early in measurement-based care, while others tracked enrollment and utilization without systematic outcome data. For employers, the proliferation of point solutions created coordination problems – the average large employer ended up managing several separate behavioral health vendors with limited ability to navigate members across levels of care.

From Access to Accountability

Over the last few years, the market has adjusted accordingly. Today, payers (e.g., health plans) and self-insured employers have begun conditioning contracts on measurement-based care — standardized outcome scales like PHQ-9 and GAD-7, functional improvement data, and documented reductions in downstream medical costs. The commercial model is shifting from per-member-per-month subscription structures toward outcome-tied arrangements: case rate contracts, performance guarantees, and capitated structures that align vendor economics with clinical results rather than enrollment volume.

As a result of the shifting priorities from stakeholders, some first-generation companies have struggled to keep pace. Behavioral health MA jumped 42% in 2025 – the most active year since 2022. We now see three distinct consolidation logics reshaping the market simultaneously: (1) platform aggregation like Spring Health’s acquisition of Alma which combines employer mental health delivery with clinician network infrastructure and payer contracting, (2) health system entry such as UHS’ $835 million acquisition of Talkspace which signals traditional inpatient systems buying virtual delivery channels as a direct response to the workforce shortage, and (3) capability bolt-ons, demonstrated by Noto’s acquisition of Rebound Health, which expanded its specialty therapy platform to include PTSD and Trauma. The fragmented point-solution era is ending. Integrated platforms combining clinical delivery, clinician networks, measurement-based care, and payer contracting are building scale advantages that standalone point solutions cannot replicate.

For health plans, health systems, and employers, the consolidation wave is both an opportunity and a decision point. The platforms building payer relationships and outcomes infrastructure today will have structural contracting advantages that are difficult to overcome later. Partnership decisions made in the next 12 to 24 months will shape which platforms have the network depth and clinical evidence to be viable long-term partners. Two examples illustrate what early, deliberate partnership decisions look like in practice. Evernorth, Cigna’s health services division, partnered with and invested in Octave to build a scalable, measurement-based care infrastructure, growing from 1,000 to 5,000 providers in 18 months and reporting an 84% reduction in depression and anxiety symptoms. Cigna separately partnered with Headspace to extend the care continuum, giving more than 7 million members access to app-based mental health support. Memorial Hermann, facing high-acuity patients arriving in emergency settings with no transitional care options, partnered with Charlie Health to provide virtual intensive outpatient programs, directly targeting the readmission cycle that drives costs. Together, these partnerships reflect a broader shift: health systems and payers are selecting partners not on access metrics alone, but on clinical capacity, care continuum coverage, and measurable outcomes.

Technology Enabling the Next Generation of Behavioral Health Care

The behavioral health workforce crisis is not a temporary imbalance and projected shortages over the next 10 years demonstrate that the supply gap is worsening. Technology is not an efficiency option in this environment — it is a structural necessity.

AI has emerged as the primary lever. Among select behavioral health organizations, AI adoption nearly doubled from 15% in 2024 to 29% in 2025, with clinical documentation and administrative automation leading the way. Ambient documentation tools reduce the time clinicians spend on progress notes, treatment plans, and billing — directly addressing the administrative burden that drives burnout and limits panel size. AI-driven triage and care routing tools match patients to the right level of care faster and more accurately than traditional intake processes, reducing time-to-care and improving patient-provider fit. Continuous outcomes monitoring platforms flag deterioration, medication non-adherence, and engagement risk before they escalate. These capabilities extend what existing providers can do — allowing a constrained workforce to manage more patients without sacrificing clinical quality. For example, Noto, has built the infrastructure layer to transform specialty care at scale: its AI-powered platform supports specialty & condition-specific therapy brands, including NOCD (OCD) and Rebound Health (PTSD and Trauma), by driving payer partnerships, enabling strong enrollment campaigns, and power treatment operations.

Consumer-facing AI is also maturing, but meaningful questions about clinical oversight, safety, and generalizability remain. A 2025 randomized controlled trial of Therabot (Dartmouth) demonstrated clinically significant reductions in depression and anxiety, with effect sizes approaching those of first-line psychotherapy. The researchers emphasized that clinician oversight and validation in larger, more diverse samples are necessary before autonomous deployment at scale. These results are opening a new conversation about coverage pathways for clinically validated AI tools as a workforce multiplier for lower-acuity populations, but it’s critical that a licensed clinician remains accountable for diagnosis and escalation.

The critical distinction the market is drawing today is between supervised AI and autonomous AI. Supervised tools — where a licensed clinician remains accountable for diagnosis, treatment, and escalation — are currently winning payer confidence, navigating FDA’s Software as a Medical Device framework more successfully, and generating the reimbursement traction that autonomous chatbots without clinical oversight have yet to today. For now, the platforms investing in supervised regulatory compliance and clinical validation are building a durable advantage.

The Digital Behavioral Health Market Landscape

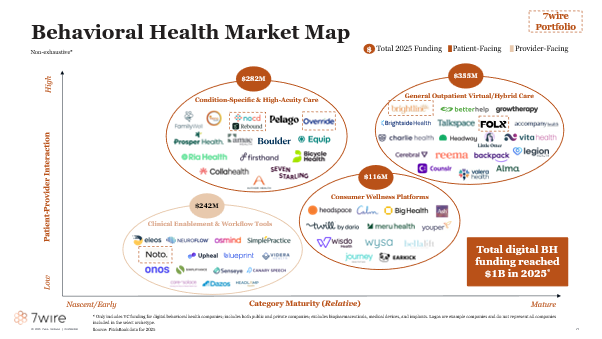

Digital behavioral health funding is entering a maturation phase: total funding reached approximately $1 billion in 2025, with average deal size roughly doubling from $12 million to $25 million with capital concentrating within scaled, outcomes-proven platforms rather than early-stage access plays. We organize the market into four segments.

General Outpatient Virtual and Hybrid Care ($335M in 2025 funding). Platforms delivering routine outpatient therapy and psychiatry via telehealth or hybrid models, including provider directories matching patients to in-network clinicians. Competition has shifted from access to clinical model depth: evidence-based therapeutic delivery, prescribing capability, outcomes measurement, and payer contracting sophistication are now table stakes. Notable companies include:

- Brightline: Delivers pediatric and young adult mental health care through therapy, psychiatry, and psychological testing via a virtual and in-person hybrid model, with AI embedded across provider productivity, member access, and operations.

- Headway: Insurance-based therapist marketplace that simplifies in-network credentialing and billing for independent clinicians, expanding affordable access to outpatient mental health care,

- Talkspace: Telehealth platform offering therapy and psychiatry across consumer, employer, and health plan channels, recently acquired by UHS as traditional health systems move into virtual behavioral health delivery,

Condition-Specific and High-Acuity Care ($282M in 2025 funding). Specialized programs targeting defined diagnoses or serious mental illness, combining virtual psychiatry and therapy, peer support, and intensive care coordination. This segment is increasingly defined by the payer contracting depth and outcomes evidence built around discrete conditions. Notable companies include:

- NOCD: One of the leading specialty platforms for OCD, delivering live-video Exposure Response & Prevention (ERP) therapy with licensed OCD specialists, 24/7 between-session support through the NOCD app, and coverage across 70+ insurance plans in all 50 states.

- Equip: Virtual eating disorder treatment platform delivering family-based care with multidisciplinary clinical teams and payer contracting across commercial and Medicaid plans.

- Seven Starling: Virtual perinatal mental health platform delivering therapy, group sessions, and medication management for women navigating fertility, pregnancy, and postpartum.

Consumer Wellness Platforms ($116M in 2025 funding). Direct-to-consumer self-guided apps, conversational agents, and coaching tools operating outside the clinical care setting. This segment faces the most pressure from AI-native entrants, as purpose-built foundation models trained on evidence-based therapeutic frameworks begin to demonstrate clinically meaningful outcomes in RCT settings. Coverage pathway development for clinically validated consumer AI tools is an active area of payer experimentation. Notable companies include:

- Headspace: Meditation and mental wellness app now partnering with Cigna to extend coverage to more than 7 million members, with bidirectional referral pathways to in-network clinical care.

- Calm: Consumer mindfulness and sleep platform expanding into employer and payer channels as a lower-acuity entry point to the behavioral health care continuum.

- Big Health: Digital therapeutics company delivering clinically validated, prescription-grade programs for insomnia and anxiety as an alternative to medication.

Clinical Enablement and Workflow Tools ($242M in 2025 funding). Provider-facing software that surfaces clinical insights, supports measurement-based care, and automates documentation and administrative workflows. This is the highest-growth segment by investment velocity, reflecting the market’s recognition that solving the supply constraint is as economically valuable as building the next consumer-facing platform. Notable companies include:

- Eleos Health: Ambient documentation and clinical intelligence platform for behavioral health providers, reducing note-writing time and surfacing outcomes data to support measurement-based care.

- Blueprint: Measurement-based care platform that automates outcome scale administration, progress tracking, and treatment planning for outpatient behavioral health practices.

- Osmind: AI-native EHR, billing, and care network purpose-built for interventional psychiatry, supporting Spravato, TMS, ketamine, and other emerging modalities across a network of 1,000+ independent practices nationwide.

Perspectives from Key Opinion Leaders

To ground these themes in practitioner and payer experience, we convened a panel of three leaders at the forefront of behavioral health delivery and innovation: Dr. Thomas Insel, former Director of the National Institute of Mental Health and Co-founder and President of Benchmark Health; Corbin Petro, President of Carelon Behavioral Health and the founder of Eleanor Health; and Stephen Smith, Co-founder and CEO of Noto. The conversation reinforced a through-line running across all three perspectives: the behavioral health industry has historically optimized for generalist access, and is now in a phase of optimizing for specialty access and outcomes. Panelists noted that while access expansion was a necessary paradigm during the pandemic and shortly thereafter, the lack of standardized outcome measurement and clinical accountability allowed many companies to scale utilization without connecting people to evidence-based, specialty treatments that drove outcomes. From the payer side, the panel pointed to longitudinal outcome data – connecting clinical improvement to reduced downstream utilization – as the missing link between vendor contracts and demonstrable ROI. And from the delivery side, the panel underscored that quality and scale are not in tension: building outcome infrastructure from the beginning is what enables a specialty platform to grow without sacrificing clinical fidelity. The panel’s collective message aligned with where the market is heading – accountability is not a constraint on behavioral health’s potential. It is the condition for realizing it.

7wire Ventures Predictions

- Technology-enabled workforce extension will emerge as the defining investment theme in behavioral health. The provider shortage is structural and will not resolve within any near-to-medium-term horizon. The most scalable solution is enabling existing providers to operate more efficiently and manage larger patient panels. AI-powered documentation, triage automation, and outcomes tracking tools are reducing the administrative burden that drives burnout and limits panel size — directly expanding effective clinical capacity without requiring new provider supply. Expect dedicated investment in behavioral health provider enablement as a distinct category, separate from care delivery platforms, as the market recognizes that solving the supply constraint is as economically valuable as building the next consumer application. Consumer-facing AI tools with clinical validation will begin to find coverage pathways as payers recognize their potential as a workforce multiplier for lower-acuity populations.

- Outcomes data will become the primary basis for payer and employer contract decisions — reshaping which companies win. Platforms with peer-reviewed ROI and payer network depth will continue to consolidate market share as utilization-focused platforms restructure or exit. Measurement-based care will shift from a differentiator to a baseline requirement: platforms that cannot generate standardized outcome data will be excluded from value-based contracts across both payer and employer channels. For health plans, the shift toward outcomes-tied contracting will also drive consolidation of vendor relationships — from fragmented point solutions toward fewer, more accountable platform partners.

- Behavioral health integration into whole-person care models will become economically mandatory, not clinically aspirational. As Medicare Advantage penetration grows and value-based contracts place providers at financial risk for total cost of care, untreated behavioral health comorbidities become directly attributable to medical spend. The Collaborative Care Model — embedding behavioral health into primary care through structured screening, care management, and psychiatric consultation — will see broader adoption as reimbursement pathways mature and workflow integration barriers decrease. Platforms that can manage behavioral health alongside metabolic and chronic physical conditions will be preferentially contracted as the cardio-kidney-metabolic framework gains commercial traction.Behavioral health is not a niche clinical category. It is among the fastest-growing cost drivers in American healthcare, deeply entangled with every chronic condition that payers and health systems struggle to manage. The first wave of digital innovation proved that technology could expand access. The next wave will prove that technology can drive accountability — that people get better, that costs come down, and that the platforms delivering those outcomes can be measured, contracted, and trusted. At 7wire Ventures, we are closely tracking the companies building the infrastructure for that accountability era, and we believe the next generation of behavioral health platforms will be defined not by how many people they can enroll, but by the outcomes they can demonstrate and the system relationships they have earned.

Behavioral health is not a niche clinical category. It is among the fastest-growing cost drivers in American healthcare, deeply entangled with every chronic condition that payers and health systems struggle to manage. The first wave of digital innovation proved that technology could expand access. The next wave will prove that technology can drive accountability — that people get better, that costs come down, and that the platforms delivering those outcomes can be measured, contracted, and trusted. At 7wire Ventures, we are closely tracking the companies building the infrastructure for that accountability era, and we believe the next generation of behavioral health platforms will be defined not by how many people they can enroll, but by the outcomes they can demonstrate and the system relationships they have earned.

If you are building and innovating in the digital behavioral health space, we welcome conversation and partnership. Reach out at investor@7wireventures.com.